3 April, 2020

Endre Pedersen, Chief Investment Officer Fixed Income, Asia ex-Japan

Concerns of a COVID-19-induced economic shock, coupled with the recent sharp decline in oil prices, introduced additional volatility and uncertainty to global and Asian financial markets. In this note, the Asian fixed-income team, led by Endre Pedersen, examines the opportunities in Asian bond markets arising from these dislocations and explains why they believe the asset class is well positioned to weather the storm.

During periods of heightened volatility, liquidity typically prevails, and market participants are unlikely to appreciate the economic and corporate fundamentals that the region’s markets have to offer. This has introduced dislocations to Asian bond markets, leading to widened Asian credit spreads and weakened Asian currencies beyond the norm.

The dynamics of Asian credit differ from developed-market credit; there are three characteristics that we feel make Asian investment-grade (IG) credit well placed to weather the impact arising from the COVID-19 outbreak. First, around 39% of the J.P. Morgan Asia Credit Index (JACI) is government or state owned:1 Asian state-owned enterprises (SOEs) typically benefit from government support, especially sectors considered to have systemic importance to the economy (e.g., oil exploration firms and utility providers). Second, most Asian issuers have the ability to issue bonds in the local currency bond market and benefit from domestic monetary policy easing measures. This also suggests that they have diversified channels of capital market funding and aren’t overly reliant on issuing US dollar-denominated debt as a source of funding. Third, Asian issuers with deep local history are typically supported by a strong and loyal investor base locally.

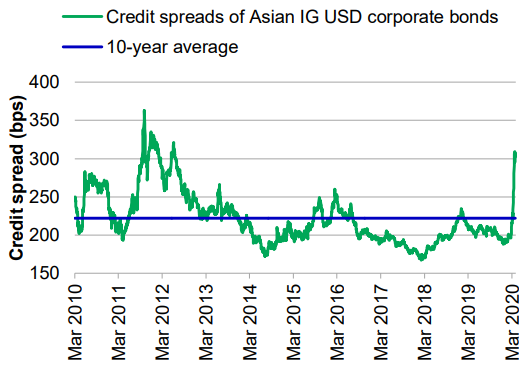

At this juncture, we believe valuations of Asian credit are increasingly attractive from a historical perspective. As of 31 March 2020, the JACI Investment Grade Corporate Index, which tracks the credit spreads of Asian investment-grade (IG) credit, has widened to 303 basis points (bps)—a level last seen in 2011/2012 during the European debt crisis—significantly above the 10-year average of 222bps.2 Notably, within the Asian IG spectrum, we believe selective SOEs from the Southeast Asia region are relatively attractive, having been subjected to indiscriminate selling by foreign investors amid heightened global market volatility. In our view, the government support factor, which acts as a cushion against the COVID-19-induced economic slowdown, is underappreciated by investors.

Takeaways from China’s NPC Meeting & upcoming drivers for Greater China equity market

In addition to the recent breakthroughs in AI and humanoid robot development, we observe other positive catalysts that further support the region’s market.

Policy Normalisation in Japan: how high will the BoJ go?

The Bank of Japan has continued to raise interest rates in an effort to "normalize" monetary policy, presenting potential opportunities for discerning investors.

Here come the tariffs: why it’s too soon to draw conclusions

The recent announcement of U.S. tariffs on key global trading partners grabbed plenty of headlines but until we get more details, it's hard to assess the global economic implications.

Source: Bloomberg, as of 31 March 2020. One hundred basis points (bps) equals one percent.

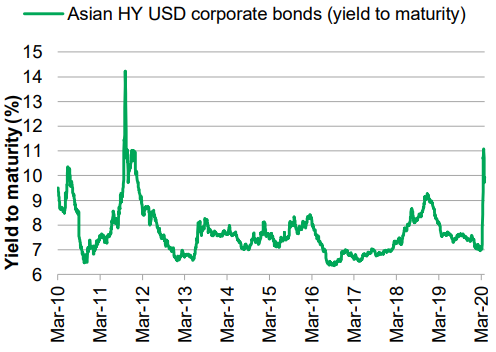

While we believe monetary easing policies introduced by Asian central banks will help prevent a systemic risk from emerging, not all companies will benefit. Against this macro backdrop, we’re increasingly selective in our credit screening process when it comes to Asian high yield (HY). We believe the current economic slowdown and lower energy prices could trigger a pickup in defaults among fundamentally weak firms within the Asian HY segment. According to our assessment, small to midsize privately owned enterprises, nonperforming state-owned enterprises, and weaker local government financing vehicles are most prone to credit defaults (sectors that we’ve generally been avoiding since 2019). Asian HY corporate bonds (as indicated by the JACI Non-Investment Grade Corporate Index) are currently offering a yield to maturity of around 10% to 11%, the highest level since 2011.2 With careful bottom-up credit selection, we think it’s possible to earn attractive returns in this space.

Source: Bloomberg, as of 31 March 2020.

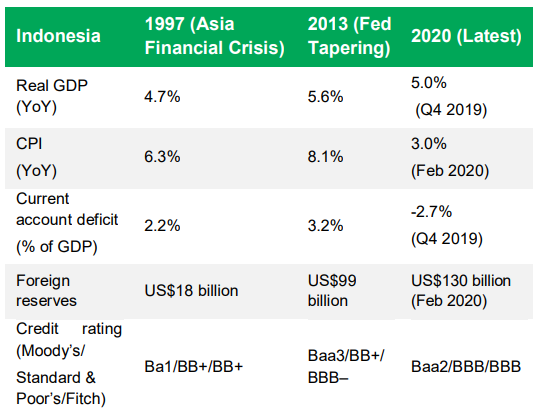

We believe the COVID-19 shock has introduced dislocations within the Asian currencies market, but to a smaller degree relative to Asian credit. Take Indonesia, for example: The Indonesian rupiah is trading near 16,000 levels (close to 1997 Asian financial crisis levels) against the US dollar (USD).2 This is primarily due to its relatively large foreign investor base (foreign investors own around 39% of the local government bond market),3 making the market prone to foreign outflows during periods of heightened global volatility. Yet Indonesia’s economic fundamentals have gradually improved over time, which can be seen in the country’s credit rating, progressively upgraded from a non-IG status in 1997 to its current IG status by all three international credit rating agencies.2 In addition, the political situation in the country has been stable, and its foreign reserves increased from US$18 billion in 1997 to US$130 billion as of February 2020.4

Source: Bloomberg, as of 31 March 2020.

In our view, the dislocated currency—at current valuation—combined with attractive yields (Indonesia’s 10-year government bond offers yields around 8%,2 the highest-yielding market within the Asian IG government bond space2) makes Indonesian bonds compelling from a total return perspective.

Nevertheless, we’re closely monitoring exogenous factors, such as changes to the US Federal Reserve’s quantitative easing program and November’s US presidential election, which will likely have an effect on the Asian currency markets.

Source: Bloomberg, as of 31 March 2020.

Asian interest rates have been relatively well behaved compared with credit and currencies. Most Asian local rate markets have seen yields drift lower year to date (with the exception of Indonesia, the Philippines, and Malaysia) amid safe haven flows.2

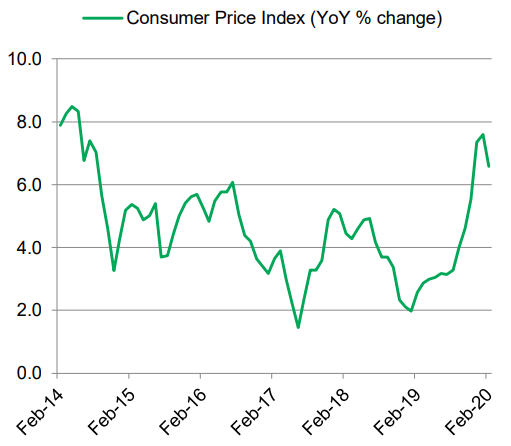

In our view, Indian local government bonds are looking increasingly interesting at this juncture. India’s headline inflation rose by 7.59% year over year (YoY) in January, but is likely to have peaked. The main driver for inflation to overshoot was higher food prices, which is expected to be transitory. Furthermore, India is a net importer of oil and can be expected to benefit from lower energy costs, which translates into an improved trade balance and lower inflation that should be supportive of the economy on a relative basis. As concerns about inflation ease, the Reserve Bank of India will have more room to resume monetary policy easing (the bank had kept interest rates on hold from October 2019 to February 2020 due to rising inflation, and resumed with a rate cut on March 27, 20202 ).

Source: Bloomberg, as of February 2020.

In our view, Asian bonds can provide potential diversification benefits for investors, thanks to the diverse makeup of Asian economies; for example, China onshore bonds were positive performing year to date among Asian bonds from a total return perspective in USD terms5 (income from coupon and bond price appreciation more than offsetting currency movements) primarily due to safe haven flows, expectations of further monetary policy easing, and increasing inclusion into global and regional bond indexes. Going forward, we believe that once markets stabilize, the sharp fall in US Treasury yields, when compared with—the now even higher—Asian yield premiums, should be broadly supportive for Asian hard and local currency bonds. In the medium term, with US Treasury yields lower, and once COVID-19 has been largely contained in Asia, liquidity conditions should normalize and help recover some of these price dislocations.

1 J.P. Morgan Asia Credit Index, as of 31 March 2020.

2 Bloomberg, as of 31 March 2020.

3 asianbondonline.abd.org, as of December 2019.

4 Bloomberg, as of 31 March 2020.

5 Bloomberg, as of 31 March 2020; based on the year-to-date performance of the Markit iBoxx ALBI China Onshore Index.

Takeaways from China’s NPC Meeting & upcoming drivers for Greater China equity market

In addition to the recent breakthroughs in AI and humanoid robot development, we observe other positive catalysts that further support the region’s market.

Policy Normalisation in Japan: how high will the BoJ go?

The Bank of Japan has continued to raise interest rates in an effort to "normalize" monetary policy, presenting potential opportunities for discerning investors.

Here come the tariffs: why it’s too soon to draw conclusions

The recent announcement of U.S. tariffs on key global trading partners grabbed plenty of headlines but until we get more details, it's hard to assess the global economic implications.

©1999 - 2025 Manulife Investment Management (Hong Kong) Limited