Macroeconomic Strategy Team

10 January 2023

As we consider the year ahead, we expect to see a game of two halves, where challenging conditions will prevail in the first half before improving through the second half. The aggressive pace of monetary tightening and its associated lagged effects should drive a synchronised global growth downturn in the first half.

We expect global growth to slow materially and come in substantially lower than the below 3% threshold that the International Monetary Fund uses to define global recessions. A downturn of this magnitude—excluding the COVID-19 shock and the global financial crisis—could make 2023 the worst year for global growth since the 1980s. We expect the economic slump to become more apparent in the first half of the year, with a cyclical bottom only occurring in Q2/Q3.

Our analysis shows that most advanced economies are likely to experience a recession in the year ahead. Given that the U.S. Federal Reserve (Fed) has been hiking rates at the fastest pace in decades, the U.S. economy will be facing the lingering effects of substantial policy tightening, with real rates rising while inflation eases gradually.

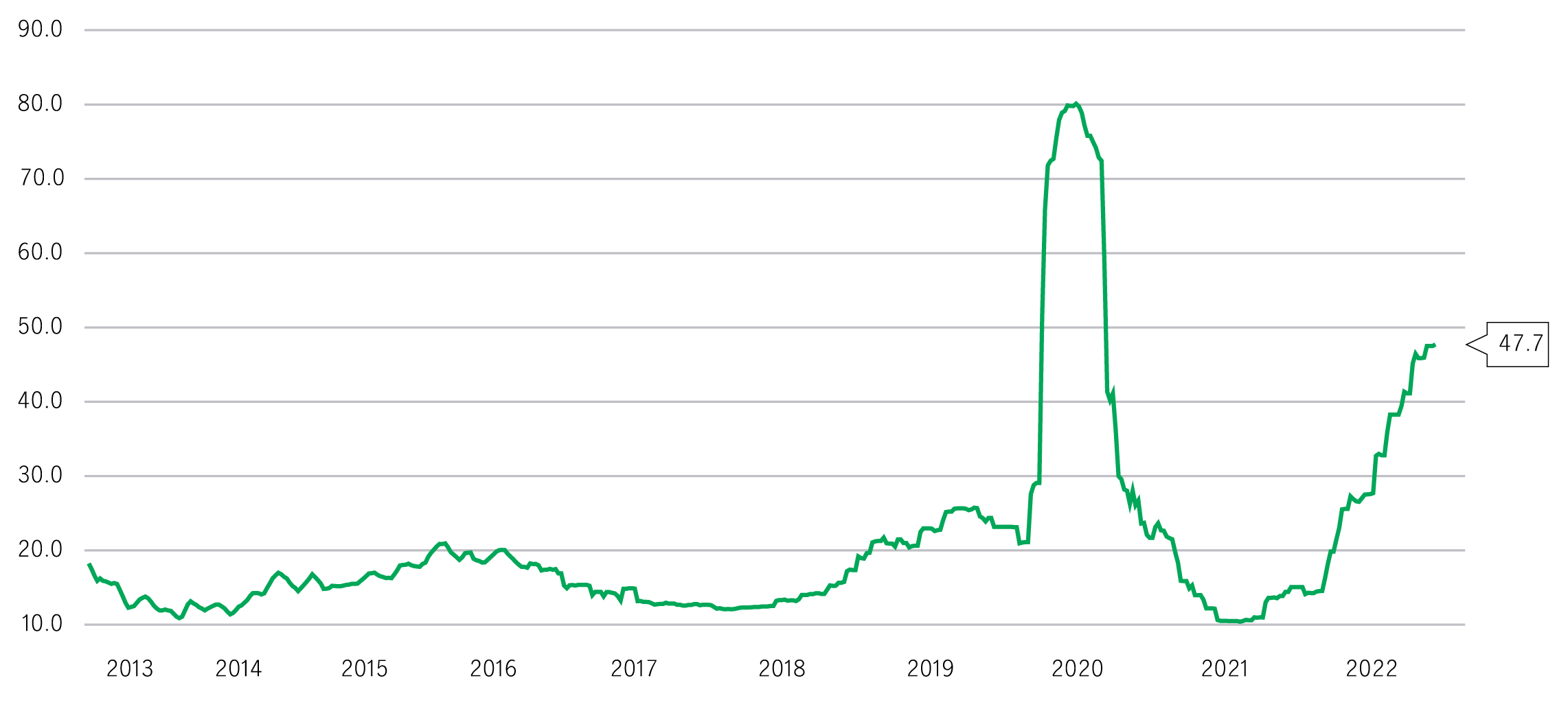

Market’s view on the probability of a global recession (%)

Source: Bloomberg, Macrobond, Manulife Investment Management, as of 13 December, 2022.

Economic weakness will be particularly pronounced in interest-rate-sensitive economies such as Canada, Australia, New Zealand, and the United Kingdom—these economies would almost certainly be confronting downside risks as a result of spillovers from their respective weaker housing markets. In Continental Europe, the growth drag will predominantly stem from particularly large negative terms-of-trade shocks.

Meanwhile, slowing final demand from advanced economies, elevated inflation, and a still-strong U.S. dollar (USD) will likely morph into material headwinds for growth in emerging markets (EM). In mainland China, a bumpy exit from zero-COVID policy, weak external demand, a still struggling property sector, and insufficient policy support look set to extend the country’s below-trend GDP into 2024. That said, the prospects for the rest of Asia’s economies are a little more mixed: We expect weak foreign demand to weigh on export growth, but North Asia is particularly vulnerable in light of a likely inventory overhang. On the other hand, weakness in ASEAN countries will likely be cushioned by a strong reopening bounce and relatively healthy household balance sheets.

Amid a macro backdrop characterized by elevated global inflation, uncertainty over when Fed rates might peak, and rising odds of a global recession, the first half of 2023 could bear witness to a series of sharper—and longer—bouts of market volatility. Thankfully, the picture does brighten slightly in the second half, during which these headwinds are likely to moderate, ushering in more conducive conditions for financial markets.

Asian Credit: Three themes should propel returns in 2H 2024

We explain how three themes should continue to support Asian credit in the second half of the year, presenting attractive opportunities for investors, particularly in the high-yield segment.

Asset allocation outlook: balance of risks tilt to the downside

Investors are navigating an environment characterized by significant global economic resilience, but with crosscurrents. We review some of the themes driving our latest asset allocation outlook.

2024 Outlook Series: Global Healthcare Equities

2023 was a tumultuous year for equity markets and the healthcare sector. For 2024, we maintain a sense of considerable optimism for the performance of healthcare equities and the underlying key subsector themes.

Asian Credit: Three themes should propel returns in 2H 2024

We explain how three themes should continue to support Asian credit in the second half of the year, presenting attractive opportunities for investors, particularly in the high-yield segment.

Asset allocation outlook: balance of risks tilt to the downside

Investors are navigating an environment characterized by significant global economic resilience, but with crosscurrents. We review some of the themes driving our latest asset allocation outlook.

2024 Outlook Series: Global Healthcare Equities

2023 was a tumultuous year for equity markets and the healthcare sector. For 2024, we maintain a sense of considerable optimism for the performance of healthcare equities and the underlying key subsector themes.

©1999 - 2024 Manulife Investment Management (Hong Kong) Limited