26 May 2021

US bank portfolio management team

With each passing quarter since the pandemic began to disrupt the economy in early 2020 and the outlook for U.S. banks was upended, the industry has managed to successfully retrench and position itself to help lead the economy’s broader recovery. Nearly all publicly traded U.S. banks have released first-quarter results as of this writing, and the industry as a whole continues to exceed our expectations. Based on our analysis, here are nine salient points about the current state of banks and the implications for equity investors.

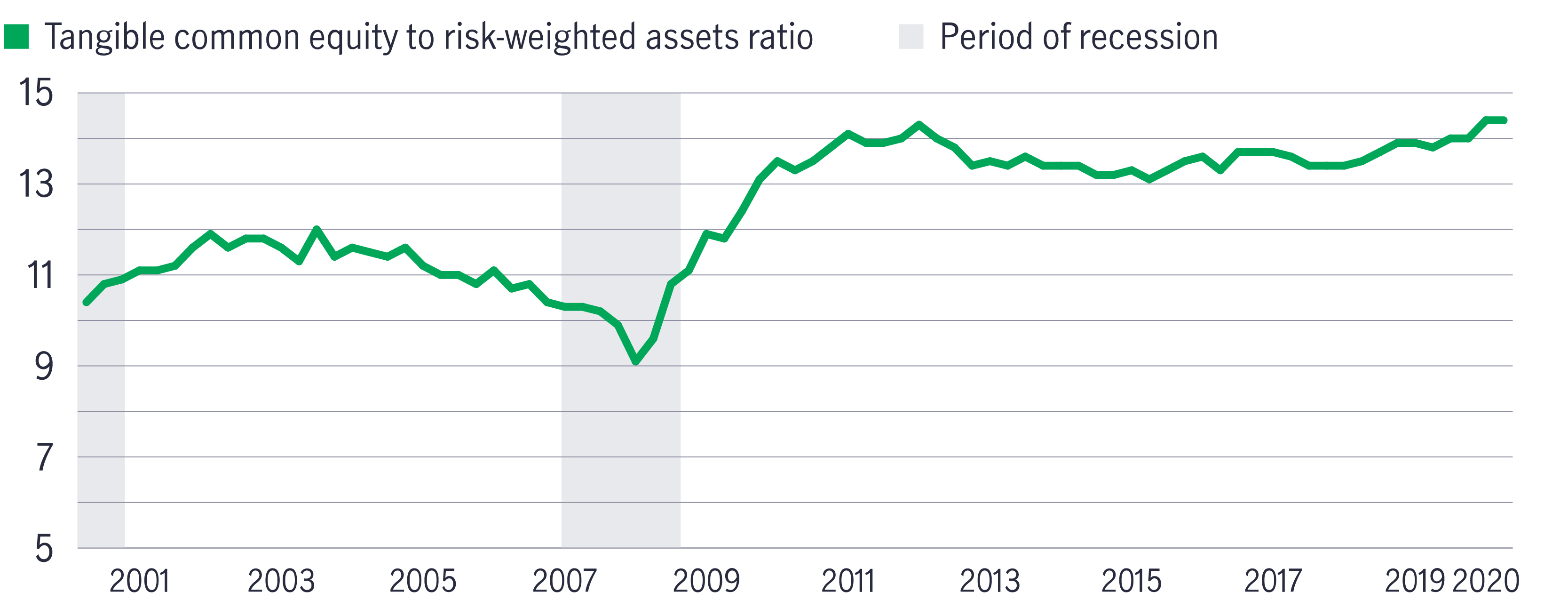

U.S. banks' capital levels have surged since a 2009 low

U.S. banks' ratio (%) of tangible common equity to risk-weighted assets, 2001–2020

Source: Federal Deposit Insurance Corp., January 2021. A tangible common equity to risk-weighted assets ratio is used to assess the potential for future bank financial stress based on commonly measured capital ratios.

U.S. banks appear to us to be fundamentally strong, with historically high levels of capital and liquidity. As the economy has reopened, credit fundamentals have been materially better than had been expected a year earlier. Strong results from regulators’ latest round of stress tests to assess major banks’ abilities to weather further economic shocks triggered a further loosening of restrictions related to share buybacks. We view these developments as a testament to the industry’s capital strength and improved underwriting. In addition, we believe that the most recent stimulus package that Congress approved in March should further support the economy and reduce credit costs. As these trends persist, we expect U.S. bank earnings to accelerate throughout 2021.

1 “KBW Bank Earnings Wrap-Up 1Q21, v. 2: Banks Continue to Deliver EPS Beats on Mostly Favorable Credit Trends,” Keefe, Bruyette & Woods, April 23, 2021.

2 Earnings per share (EPS) is a measure of how much profit a company has generated calculated by dividing the company's net income by its total number of outstanding shares.

3 U.S. Federal Reserve press release, March 25, 2021.

Better income – Preferred securities

Over the past three years, preferred securities showed slightly higher volatility than US Treasuries, but less volatile than other rate-sensitive assets like US mortgage-backed securities (MBS) and US investment-grade bonds. Preferreds also demonstrated a relatively better return than US Treasuries, MBS and investment-grade bonds.

Hong Kong/Mainland China market update

Mainland China’s Third Plenum 2024 concluded with structural reforms in key areas, and the government introduced some concrete measures. The Greater China Equities Team believes that mainland China is focusing not only on long-term structural reform but also on short-term economic targets. The series of fiscal and monetary announcements, along with greater subsidies and infrastructure spending, should support a faster recovery in domestic demand.

Better income: Global multi-asset diversified income

The Global Multi-Asset Diversified Income approach remains focused on generating higher, sustainable natural yields from a range of assets with lower correlations and expected relatively lower volatilities.

Better income – Preferred securities

Over the past three years, preferred securities showed slightly higher volatility than US Treasuries, but less volatile than other rate-sensitive assets like US mortgage-backed securities (MBS) and US investment-grade bonds. Preferreds also demonstrated a relatively better return than US Treasuries, MBS and investment-grade bonds.

Hong Kong/Mainland China market update

Mainland China’s Third Plenum 2024 concluded with structural reforms in key areas, and the government introduced some concrete measures. The Greater China Equities Team believes that mainland China is focusing not only on long-term structural reform but also on short-term economic targets. The series of fiscal and monetary announcements, along with greater subsidies and infrastructure spending, should support a faster recovery in domestic demand.

Better income: Global multi-asset diversified income

The Global Multi-Asset Diversified Income approach remains focused on generating higher, sustainable natural yields from a range of assets with lower correlations and expected relatively lower volatilities.

©1999 - 2024 Manulife Investment Management (Hong Kong) Limited